44 valuing zero coupon bonds

How Do Zero Coupon Bonds Work? - SmartAsset What Is a Zero Coupon Bond? A zero coupon bond is a type of bond that trades at a deep discount and doesn't pay interest. While some bonds start out as zero coupon bonds, others are can get transformed into them if a financial institution removes their coupons. When the bond reaches maturity, you'll get the par value (or face value) of the ... Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

Valuing a zero-coupon bond | Mastering Python for Finance - Packt A zero-coupon bond is a bond that does not pay any periodic interest except on maturity, where the principal or face value is repaid. Zero-coupon bonds are also called pure discount bonds. A zero-coupon bond can be valued as follows: Here, is the annually compounded yield or rate of the bond, and is the time remaining to the maturity of the bond.

Valuing zero coupon bonds

How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816) Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep To calculate the price of a zero-coupon bond - i.e. the present value (PV) - the first step is to find the bond's future value (FV), which is most often $1,000. The next step is to add the yield-to-maturity (YTM) to one and then raise it to the power of the number of compounding periods. What Is a Zero-Coupon Bond? Definition, Advantages, Risks As of November 2020, the current yield-to-maturity rate on the PIMCO 25+ year zero-coupon bond ETF, a managed fund consisting of a variety of long-term zeros, is 1.54%. The current yield on a...

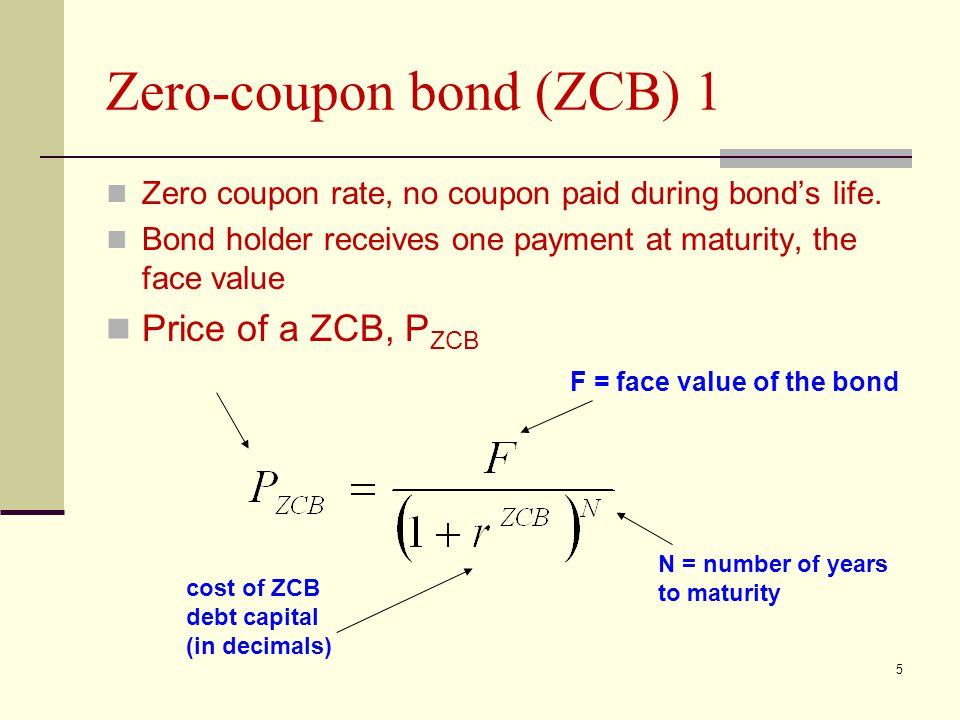

Valuing zero coupon bonds. Zero Coupon Bond Value Formula - Crunch Numbers Price of the zero-coupon bond is calculated much easier than a coupon bond price since there are no coupon payments. It is calculated as: P = \frac {M} { (1 + r)^ {n}} P = (1+r)nM Where P is the current price of a bond, M is the face or nominal value, r is the required rate of interest, n is the number of years until maturity. PDF Numerical Example in Valuing Zero coupon Bonds - New York University For example, the value of a zero coupon bond will increase from $385.00 to $620.92 as the bond moves from 10 years to maturity to 5 years to maturity assuming interest rates remain at 10%. 4) Compare the value of the zero at 10 years to maturity when rates are 10% versus when they are 7%. Lower interest rates mean higher bond prices. Zero - Coupon Bonds - Economy Blatt Zero - coupon bonds are also called pure discount bonds as they trade at a discount, a price lower than the face value prior to its maturity date. Suppose you have purchased a one - year, risk - free, zero coupon bond which has an initial price of $ 144,927. The face value of the bond is $150,000. en.wikipedia.org › wiki › Bootstrapping_(finance)Bootstrapping (finance) - Wikipedia In finance, bootstrapping is a method for constructing a (zero-coupon) fixed-income yield curve from the prices of a set of coupon-bearing products, e.g. bonds and swaps.. A bootstrapped curve, correspondingly, is one where the prices of the instruments used as an input to the curve, will be an exact output, when these same instruments are valued using this curve.

quizlet.com › 389988684 › finance-2000-chapter-7Finance 2000 Chapter 7 Valuing Bonds Flashcards | Quizlet you want to compute the value of a 5 year, zero-coupon corporate bond given a market rate of 5.5%. what are your inputs? FV=$1000 (the assumed par value of a corporate bond is $1000) Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months. Zero Coupon Bond | Investor.gov Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due. The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. Valuing Zero-Coupon Bonds A zero-coupon bond is one that does not pay interest over the term of the bond. Instead, the entity will sell the bond at lower than face value. When the bond's term is over, the issuing business will repay the bond at its face value. The bondholder generates a return paying less than what he receives in payment at the end of the bond's term.

yeson30.org › aboutAbout Our Coalition - Clean Air California About Our Coalition. Prop 30 is supported by a coalition including CalFire Firefighters, the American Lung Association, environmental organizations, electrical workers and businesses that want to improve California’s air quality by fighting and preventing wildfires and reducing air pollution from vehicles. The One-Minute Guide to Zero Coupon Bonds | FINRA.org will likely fall. Instead of getting interest payments, with a zero you buy the bond at a discount from the face value of the bond, and are paid the face amount when the bond matures. For example, you might pay $3,500 to purchase a 20-year zero-coupon bond with a face value of $10,000. After 20 years, the issuer of the bond pays you $10,000. Zero Coupon Bond: Formula & Examples - Study.com The zero-coupon bond definition is a financial instrument that does not pay interest or payments at regular frequencies (e.g. 5% of face value yearly until maturity). Rather, zero-coupon bonds ... Zero Coupon Bond Calculator - What is the Market Value? A zero coupon bond is a bond which doesn't pay any periodic payments. Instead it has only a face value (value at maturity) and a present value (current value). The entire face value of the bond is paid out at maturity. It is also known as a deep discount bond. Benefits and Drawbacks of Zero Coupon Bonds

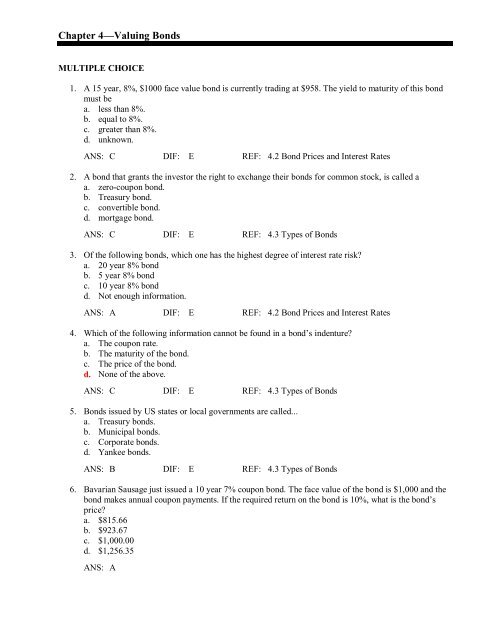

Chapter 4—Valuing Bonds - Userpage

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19.

Valuing Securities Stocks and Bonds. Bond Cash Flows, Prices ...

en.wikipedia.org › wiki › Bond_durationBond duration - Wikipedia The zero-coupon bond will have the highest sensitivity, changing at a rate of 9.76% per 100bp change in yield. This means that if yields go up from 5% to 5.01% (a rise of 1bp) the price should fall by roughly 0.0976% or a change in price from $61.0271 per $100 notional to roughly $60.968.

RBI orders five banks to list zero coupon bonds at "fair ...

Zero Coupon Bonds Explained (With Examples) - Fervent Valuing Zero Coupon Bonds on Excel® We'll be using Excel's "PRICE" function to value Swindon Plc's bond. The first thing you want to do is setup your spreadsheet with a pro-forma / template that consists of the all different variables you'll need. The "PRICE" function on Excel® requires:

Interest Rate Models for Pricing Zero Coupon Bond Options (Paperback)

Value and Yield of a Zero-Coupon Bond | Formula & Example - XPLAIND.com The bonds were issued at a yield of 7.18%. The forecasted yield on the bonds as at 31 December 20X3 is 6.8%. Find the value of the zero-coupon bond as at 31 December 2013 and Andrews expected income for the financial year 20X3 from the bonds. Value (31 Dec 20X3) =. $1,000. = $553.17. (1 + 6.8%) 9. Value of Total Holding = 100 × $553.17 ...

How to Calculate PV of a Different Bond Type With Excel

Valuation of Zero-Coupon Bonds - YouTube This video provides an explanation of a zero-coupon bond and proceeds to show how the value and yield are calculated using manual computations as well as wit...

Zero Coupon Bonds - Financial Edge

Zero-Coupon Bond Value | Formula, Example, Analysis, Calculator The zero-coupon bond value refers to the current value of a zero-coupon bond. This formula requires three variables: face value, interest rate and the number of years to maturity. The zero-coupon bond value is usually expressed as a monetary amount. This equation is sensitive to interest rate fluctuations.

Zero Coupon Bonds Explained (With Examples) - Fervent ...

› newsletters › entertainmentCould Call of Duty doom the Activision Blizzard deal? - Protocol Oct 14, 2022 · Hello, and welcome to Protocol Entertainment, your guide to the business of the gaming and media industries. This Friday, we’re taking a look at Microsoft and Sony’s increasingly bitter feud over Call of Duty and whether U.K. regulators are leaning toward torpedoing the Activision Blizzard deal.

YIELDS TO MATURITY ON ZERO-COUPON RONDS

Zero Coupon Bond Calculator - Nerd Counter Zero-Coupon Bond Yield = F 1/n PV - 1 Here; F represents the Face or Par Value PV represents the Present Value n represents the number of periods I feel it necessary to mention an example here that will make it easy to understand how to calculate the yield of a zero-coupon bond.

Lattice tree for valuing a 2-year defaultable zero coupon ...

How to Buy Zero Coupon Bonds | Finance - Zacks The bonds are sold at a deep discount, and the principal plus accrued interest is paid at the bond's maturity date. The less you pay for a zero coupon bond, the higher the yield. A bond with a ...

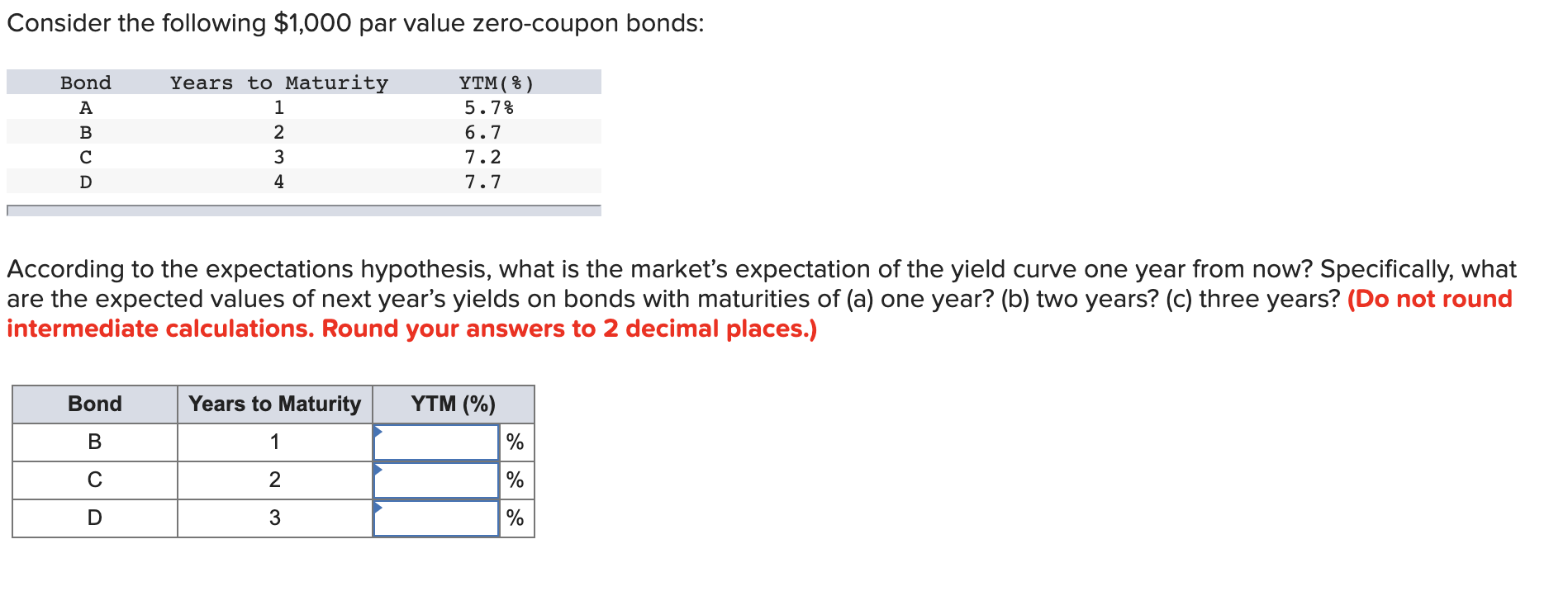

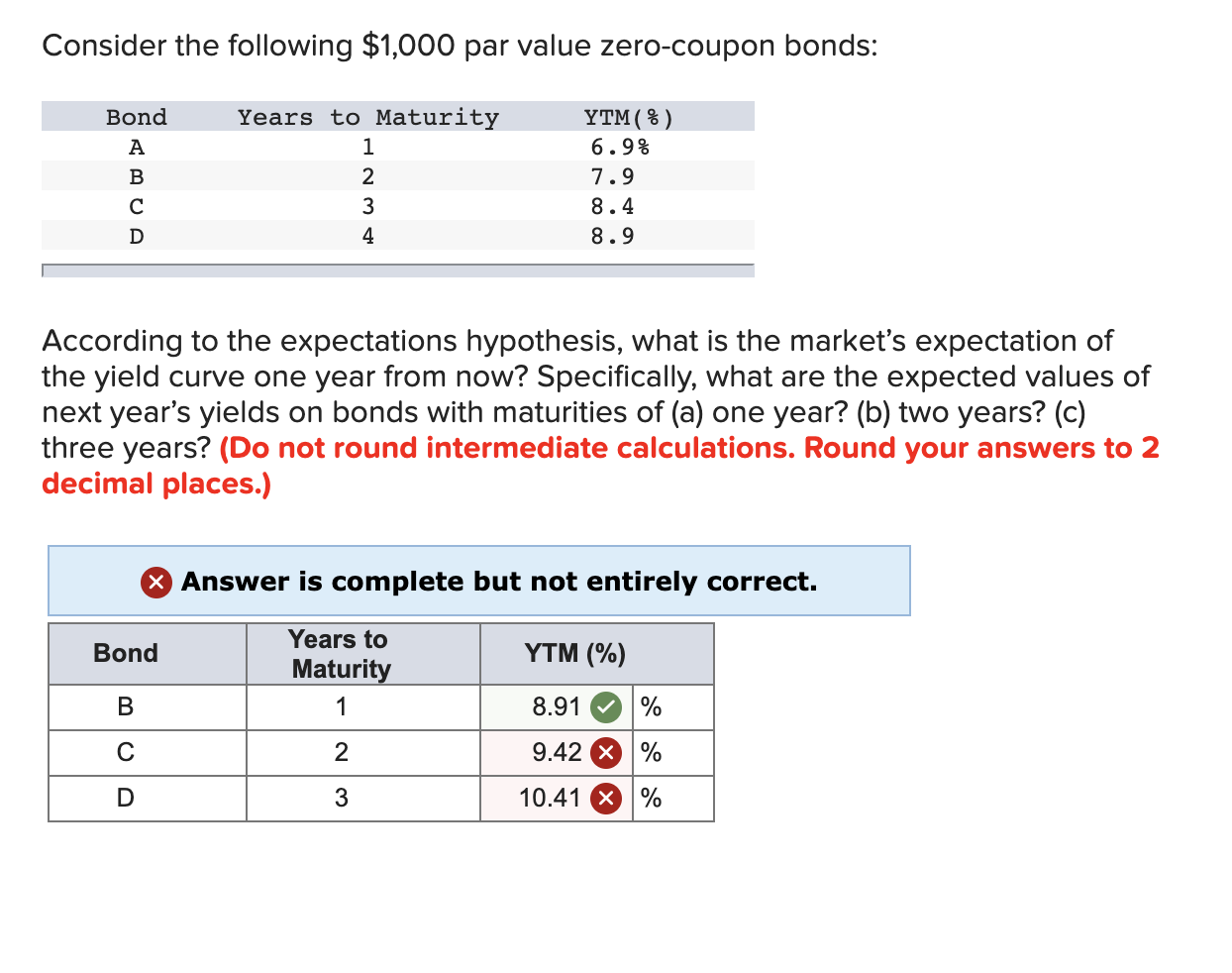

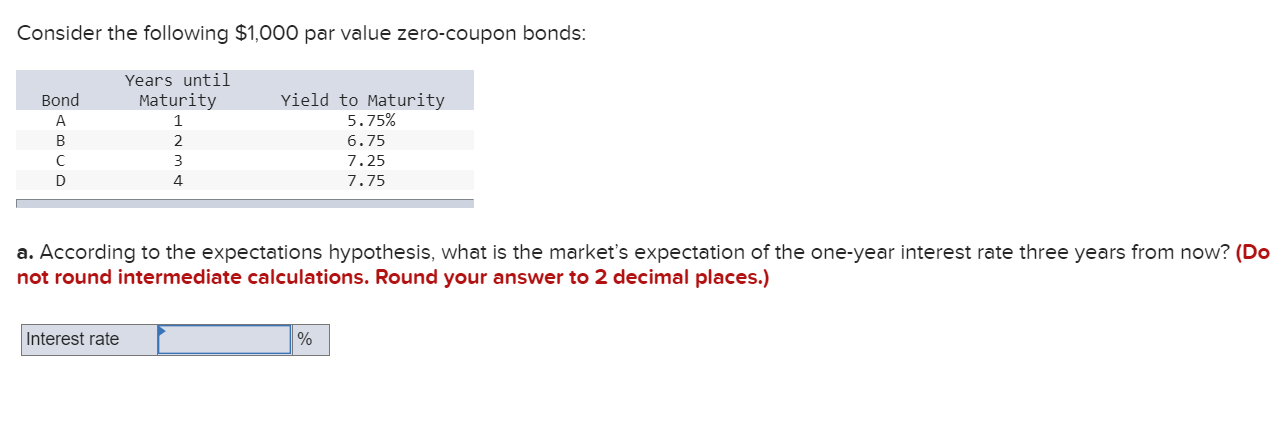

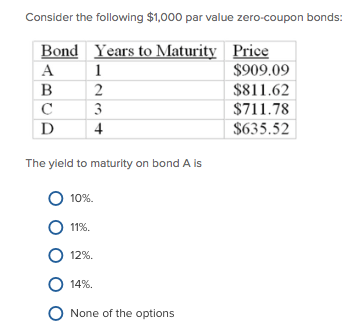

Solved Consider the following $1,000 par value zero-coupon ...

RBI orders five banks to list zero coupon bonds at "fair value" A zero-coupon bond is not an interest bearing security. Unlike other bonds, it does not pay interest regularly. These are issued at deep discounts to their face value and are redeemed at face value on the maturity date. For example, a Rs 100 face value bond maturing in 10 years could be issued at Rs. 55.

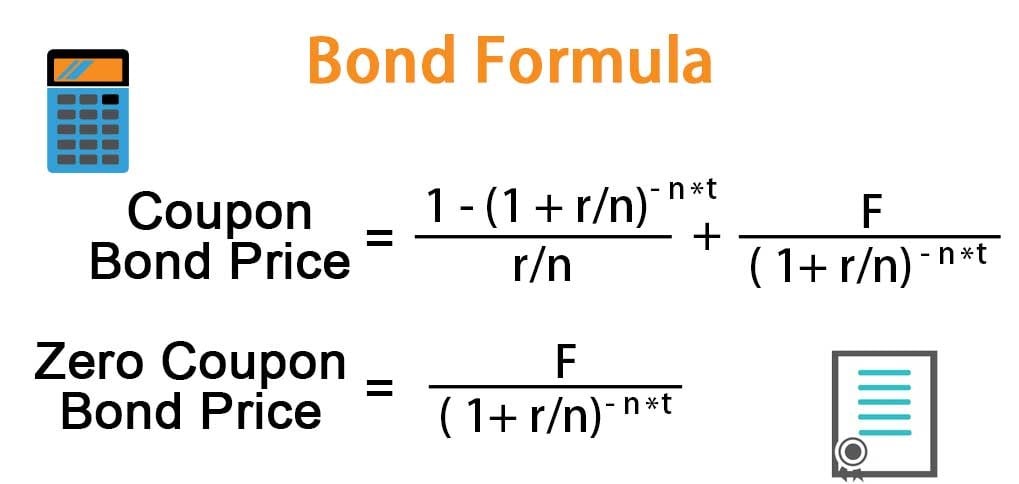

Bond Formula | How to Calculate a Bond | Examples with Excel ...

14.3 Accounting for Zero-Coupon Bonds - Financial Accounting This zero-coupon bond was sold for $2,200 below face value to provide interest to the buyer. Payment will be made in two years. The straight-line method simply recognizes interest of $1,100 per year ($2,200/2 years). Figure 14.11 December 31, Years One and Two—Interest on Zero-Coupon Bond at 6 Percent Rate—Straight-Line Method

Bond Valuation and Risk - ppt video online download

What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... Mr. Tee is looking to purchase a zero-coupon bond with a face value of $50 and 5 years till maturity. The interest rate on the bond is 2% and will be compounded annually. In the scenario above, the face value of the bond is $50. However, to calculate the price that needs to be paid for the bond today, the following formula is used:

1-3.3. Bond Valuation: Zero-coupon Bonds

› ctp › glossaryoftaxtermsGlossary of Tax Terms - OECD DEEP DISCOUNT BOND -- See: Zero coupon bond DEFAULT -- The failure of a debtor to make timely payments of interest and principal amounts as they come due or to meet some other provision of a bond, mortgage, lease, or other contract. DEFERMENT OF TAX -- The postponement of tax payments from the current year to a later year. A number of countries ...

How to Calculate a Zero Coupon Bond Price | Double Entry ...

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

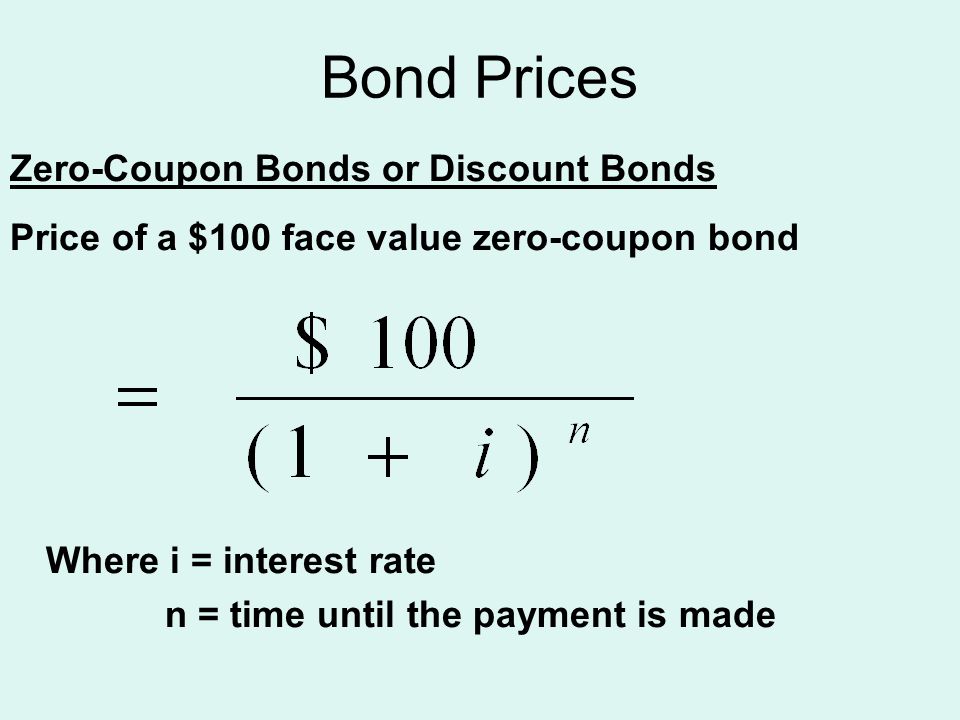

Bond Prices Zero-coupon bonds: promise a single future ...

What Is a Zero-Coupon Bond? - Investopedia A zero-coupon bond is a debt security instrument that does not pay interest. Zero-coupon bonds trade at deep discounts, offering full face value (par) profits at maturity. The difference...

Solved] Show that the no-arbitrage time-zero value of a zero ...

Advantages and Risks of Zero Coupon Treasury Bonds - Investopedia General Advantages of Zero-Coupon Bonds Why would anyone want a bond without the interest? Well, for one thing, zero-coupon bonds are bought for a fraction of face value. For...

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

en.wikipedia.org › wiki › Short-rate_modelShort-rate model - Wikipedia The interest rates implied by the zero coupon bonds form a yield curve, or more precisely, a zero curve. Thus, specifying a model for the short rate specifies future bond prices. This means that instantaneous forward rates are also specified by the usual formula

Zero Coupon Bonds Explained (With Examples) - Fervent ...

What Is a Zero-Coupon Bond? Definition, Advantages, Risks As of November 2020, the current yield-to-maturity rate on the PIMCO 25+ year zero-coupon bond ETF, a managed fund consisting of a variety of long-term zeros, is 1.54%. The current yield on a...

PPT - Chapter 5: Bond and Stock (Equity) Valuation PowerPoint ...

Zero-Coupon Bonds: Characteristics and Examples - Wall Street Prep To calculate the price of a zero-coupon bond - i.e. the present value (PV) - the first step is to find the bond's future value (FV), which is most often $1,000. The next step is to add the yield-to-maturity (YTM) to one and then raise it to the power of the number of compounding periods.

Zero Coupon Bonds Explained (With Examples) - Fervent ...

How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816)

Bond Valuation II – Zero-Coupon Bonds – From First Principles

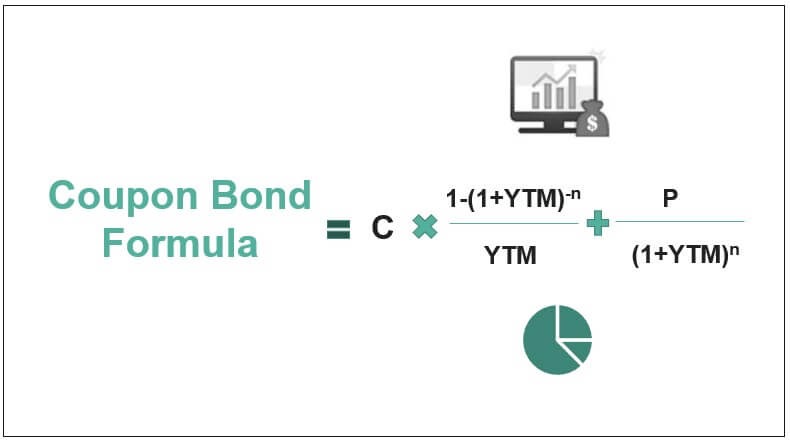

Coupon Bond Formula | Examples with Excel Template

WWWFinance - Bond Valuation: Campbell R. Harvey

Zero Coupon Bond Valuation and Risk - ppt download

Zero Coupon Bonds

How to calculate bond price in Excel?

Valuing bonds. (Lecture 6) - презентация онлайн

Calaméo - Understanding Zero Coupon Bond Product and Pricing

Solved Consider the following $1,000 par value zero-coupon ...

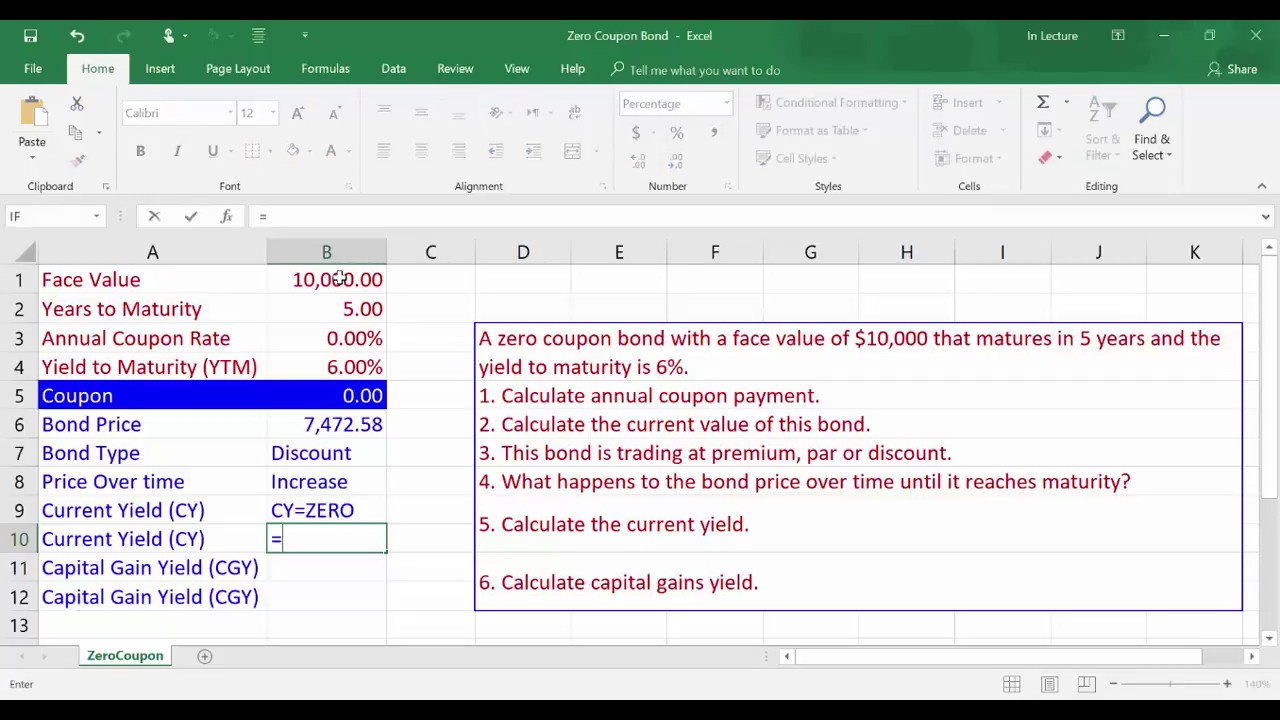

Zero Coupon Bond Valuation using Excel

Valuing a zero-coupon bond | Mastering Python for Finance ...

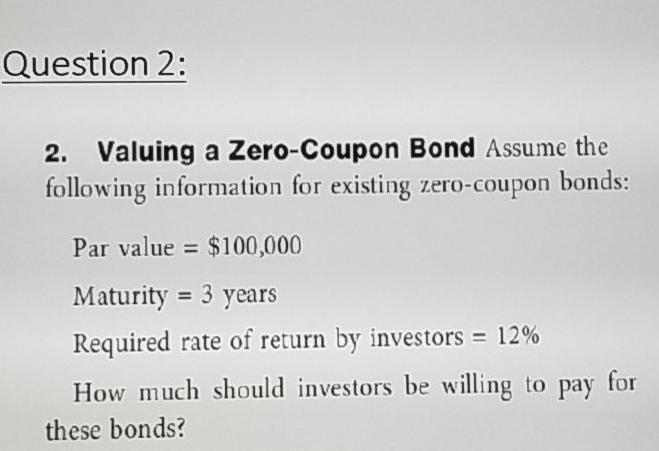

Solved Question 2: 2. Valuing a Zero-Coupon Bond Assume the ...

Calculating the Yield of a Zero Coupon Bond using Forward Rates

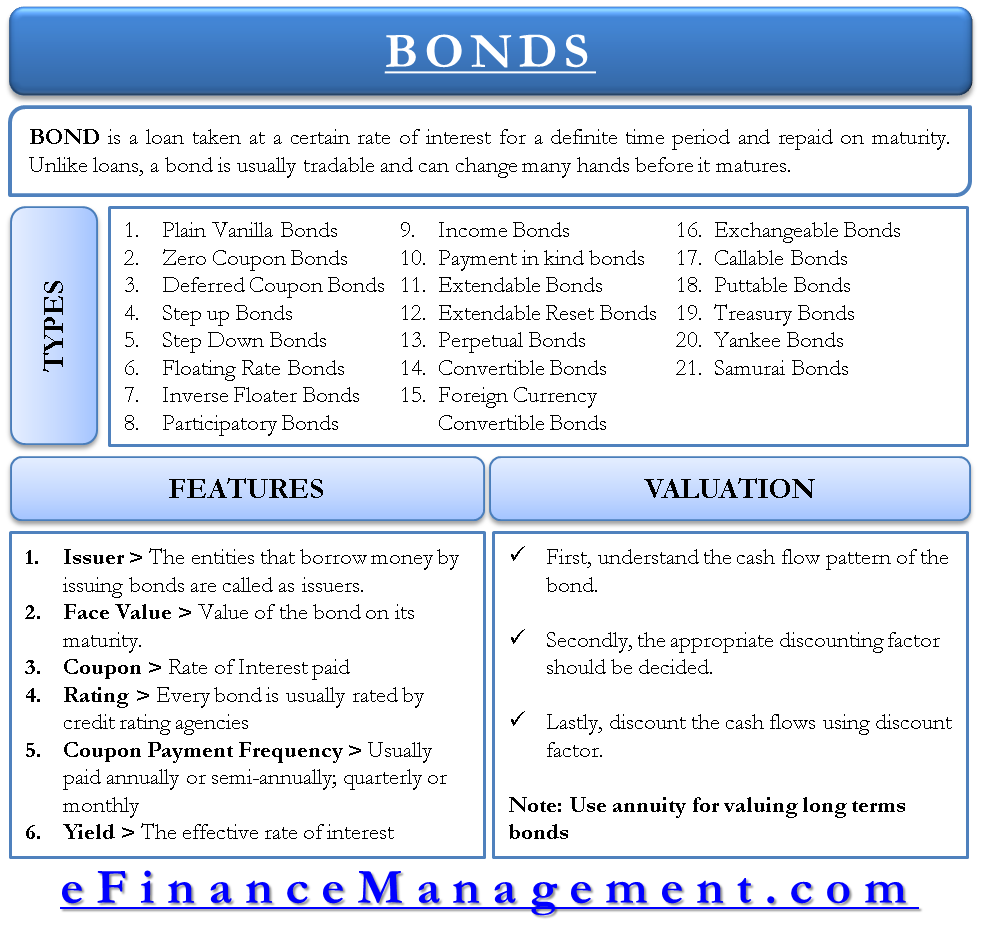

All the 21 Types of Bonds | General Features and Valuation | eFM

Coupon Bond Formula | How to Calculate the Price of Coupon Bond?

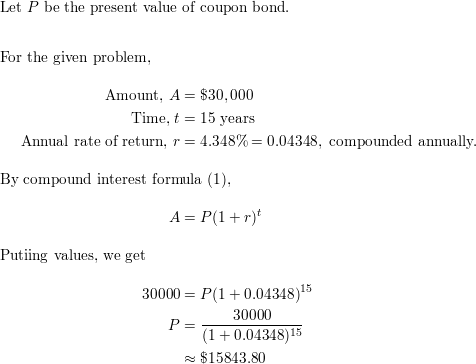

A zero coupon bond with a face value of $30,000 matures in 1 ...

Solved Consider the following $1,000 par value zero-coupon ...

Bond Pricing: How to Price a Zero Coupon Bond

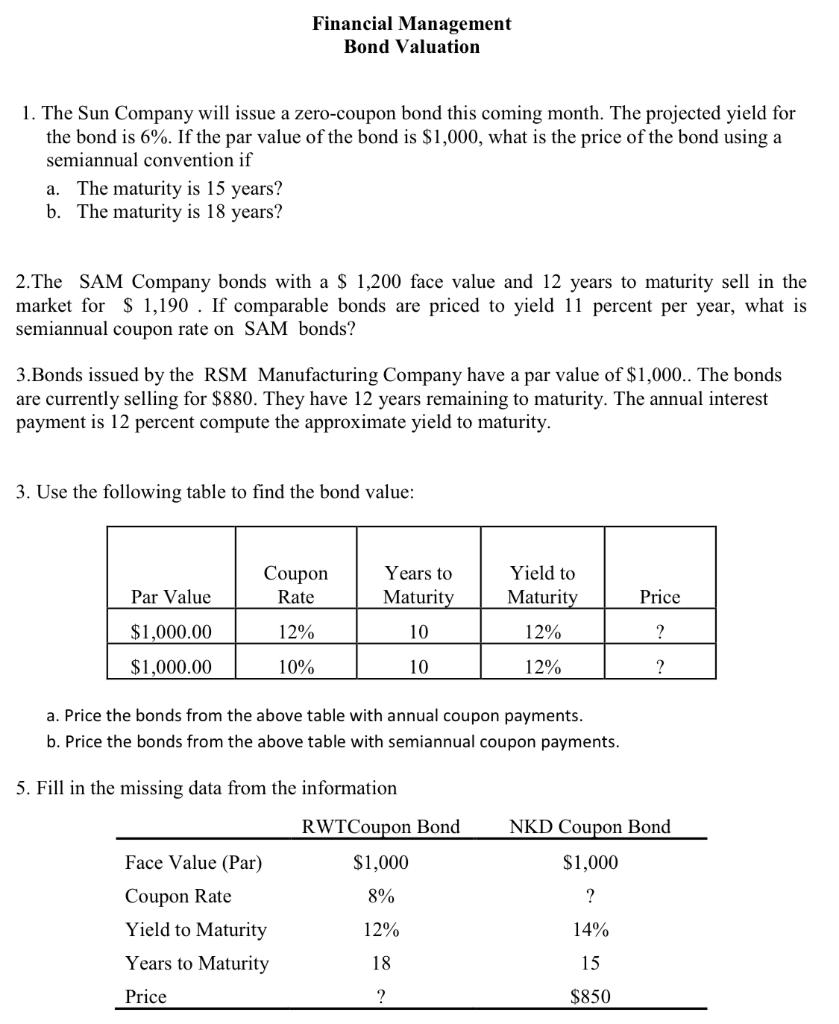

Solved Financial Management Bond Valuation 1. The Sun | Chegg.com

Solved Consider the following $1,000 par value zero-coupon ...

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

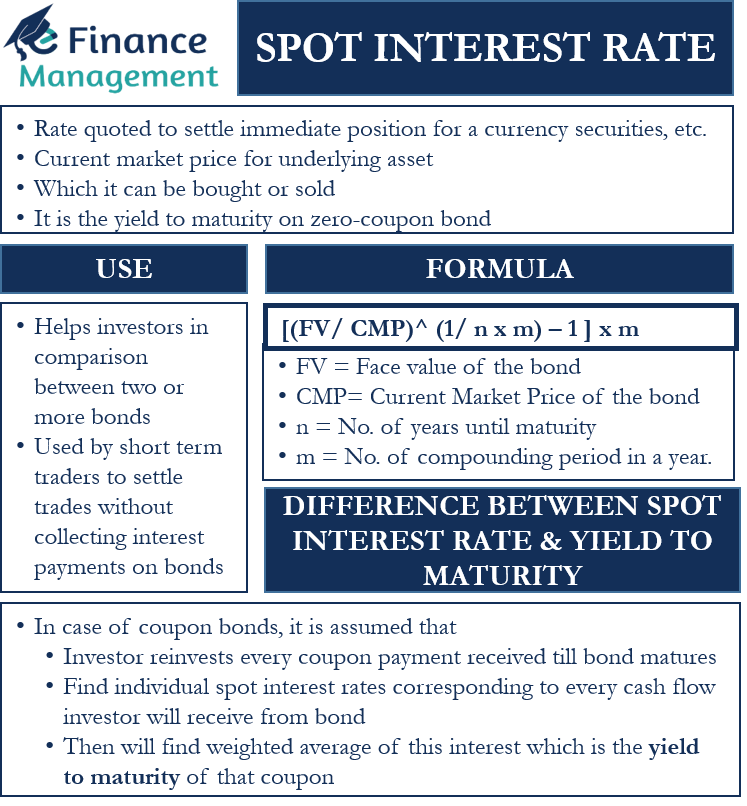

Spot Interest Rate: Meaning, Usage, Calculation, Examples

Solved JIN SHLONIK LTE * 3:12 PM @ 1 25%O 1. Valuing Bonds ...

Bond valuation

Post a Comment for "44 valuing zero coupon bonds"